Request for Proposals

Energy Tax Credit Advisory Services Issued May 20, 2026

North Georgia EMC

REQUEST FOR PROPOSALS NOTICE

For Energy Tax Credit Assistance Services

Date: May 20, 2026

Proposals are requested from professional tax advisers with a strong record in successfully assisting local governments and other entities with the implementation of projects involving IRS Energy Tax Credits and federal funds, including Appalachian Regional Commission funds. Responding firms should have the experience and capabilities necessary to ensure that energy tax credits pledged as federal cost share are properly substantiated, legally eligible, timely realized, and defensible in the event of IRS review or audit. Plans are to contract within a year from the date of this notice, with a reputable consulting firm for advisement on Federally Funded Projects related to battery energy storage system development projects.

Information that should be submitted for our evaluation is as follows:

- Firm Overview and Relevant Experience

- Relevant Project Experience

- Key Personnel and Project Team

- Technical Approach and Project Execution

- Risk Identification and Mitigation

- References

- Fees

- Statement of Qualifications

- All contracts are subject to Federal and State contract provisions prescribed by the Georgia

- Department of Community Affairs.

NGEMC also abides by the following laws as they pertain to HUD Assisted Projects: Title VI of the Civil Rights Act of 1964; Section 109 of the Housing and Community Development Act of 1974, Title 1; Title VII of the Civil Rights Act of 1968 (Fair Housing Act); Section 104(b)(2) of the Housing and Community Development Act of 1974; Section 504 of the Rehabilitation Act of 1973 as amended; Title II of the Americans with Disabilities Act of 1990 (ADA); and the Architectural Barriers Act of 1968.

Interested parties should request copies of the Statement of Qualifications Form prior to preparing and submitting their proposal. Proposals are due by 4:30 PM on July 6, 2026. Proposals received after the above date and time may not be considered. We reserve the right to accept or reject any and all proposals and to waive informalities in the proposal process. Questions, Statement of Qualifications, and proposal packages should be submitted to the two contacts listed below:

Paul Ruud,

VP Engineering Services

North Georgia E.M.C

pruud@ngemc.com

AND

Coty Burch,

Engineer

North Georgia EMC

cburch@ngemc.com

North Georgia EMC

SOLICITUD DE PROPUESTAS

Servicios de Asistencia para Créditos Fiscales de Energía

Fecha: May 20, 2026

Se solicitan propuestas de asesores fiscales profesionales con un sólido historial de éxito en la asistencia a gobiernos locales y otras entidades con la implementación de proyectos que involucren Créditos Fiscales de Energía del IRS y fondos federales, incluidos los fondos de la Appalachian Regional Commission. Las firmas que respondan deberán contar con la experiencia y las capacidades necesarias para garantizar que los créditos fiscales de energía comprometidos como parte de la participación de costos federales estén debidamente fundamentados, sean legalmente elegibles, se obtengan de manera oportuna y puedan sostenerse en caso de revisión o auditoría del IRS. Se tiene previsto contratar, dentro del plazo de un año a partir de la fecha de este aviso, a una firma consultora de buena reputación para brindar asesoría sobre proyectos financiados federalmente relacionados con proyectos de desarrollo de sistemas de almacenamiento de energía con baterías.

La información que deberá presentarse para nuestra evaluación es la siguiente:

- Descripción general de la firma y experiencia relevante

- Experiencia relevante en proyectos

- Personal clave y equipo del proyecto

- Enfoque técnico y ejecución del proyecto

- Identificación y mitigación de riesgos

- Referencias

- Honorarios

- Declaración de calificaciones

- Todos los contratos están sujetos a las disposiciones contractuales federales y estatales prescritas por el Departamento de Asuntos Comunitarios de Georgia.

NGEMC también cumple con las siguientes leyes en la medida en que se apliquen a los proyectos asistidos por HUD: Título VI de la Ley de Derechos Civiles de 1964; Sección 109 de la Ley de Vivienda y Desarrollo Comunitario de 1974, Título I; Título VIII de la Ley de Derechos Civiles de 1968 (Ley de Vivienda Justa); Sección 104(b)(2) de la Ley de Vivienda y Desarrollo Comunitario de 1974; Sección 504 de la Ley de Rehabilitación de 1973, según enmendada; Título II de la Ley de Estadounidenses con Discapacidades de 1990 (ADA); y la Ley de Barreras Arquitectónicas de 1968.

Las partes interesadas deberán solicitar copias del Formulario de Declaración de Calificaciones antes de preparar y presentar su propuesta. Las propuestas deberán recibirse a más tardar a las 4:30 p. m. del July 6, 2026. Las propuestas recibidas después de la fecha y hora antes indicadas podrán no ser consideradas. Nos reservamos el derecho de aceptar o rechazar cualquiera y todas las propuestas, así como de dispensar irregularidades informales en el proceso de propuestas. Las preguntas, la Declaración de Calificaciones y los paquetes de propuesta deberán enviarse a los dos contactos que se indican a continuación:

Paul Ruud

Vicepresidente de Servicios de Ingeniería

North Georgia E.M.C

pruud@ngemc.com

Y

Coty Burch

Ingeniero

North Georgia EMC

cburch@ngemc.com

REQUEST FOR PROPOSALS (RFP) –Energy Tax Credit Advisory Services

RFP Title: Energy Tax Credit Advisory Services

RFP Number: 051326

Issuing Organization: North Georgia EMC (NGEMC)

Issue Date: May 20, 2026

Proposal Due Date/Time: July 6, 2026, at 4:30 pm EST (Daylight Savings Time)

Submission Method: Electronic submittal via email to Paul Rudd, pruud@ngemc.com, AND Coty Burch, cburch@ngemc.com. No hardcopy submittal is required.

1. Procurement Contact and Communications

Procurement Contacts: Paul Ruud, pruud@ngemc.com, VP Engineering Services, AND Coty Burch, cburch@ngemc.com, Engineer, North Georgia E.M.C.

All inquiries and questions regarding this RFP must be submitted via email to the Procurement Contacts by the deadline stated in the Schedule: June 4, 2026. Responses will be posted by June 9, 2026.

Do not call or email other NGEMC employees or elected officials seeking answers to questions. NGEMC reserves the right to remove a Respondent from consideration for violating this restriction.

Questions and answers will be distributed through written addenda and posted for public access on the NGEMC website (https://www.ngemc.com/) and uploaded to the Georgia Procurement Registry portal.

2. Purpose / Overview

Proposals are requested from professional tax advisers with a strong record in successfully assisting local governments and other entities with the implementation of projects involving IRS Energy Tax Credits and federal funds, including Appalachian Regional Commission funds. Responding firms should have the experience and capabilities necessary to ensure that energy tax credits pledged as federal cost share are properly substantiated, legally eligible, timely realized, and defensible in the event of IRS review or audit. Plans are to contract within a year from the date of this notice, with a reputable consulting firm for advisement on Federally Funded Projects related to battery energy storage system development projects.

Scope of Work

The selected firm shall provide legal due diligence and guidance to assist the electric cooperative (“Client”) in successfully securing and maximizing 48E direct pay tax credits for its qualifying energy storage project. The scope of services should cover securing the 30% tax credit for meeting prevailing wage and apprenticeship requirements, and if applicable, +10 percentage points for meeting domestic content rules for iron, steel, and manufactured products, and/or +10 percentage points for being in an energy community. Please see Appendix D for the Scope of Work for this project.

Minimum Qualifications

Respondents must demonstrate direct, project-level experience advising on Section 48E energy tax credits and battery energy storage system projects. Firms lacking demonstrated experience in both Section 48E and battery storage projects will not be considered.

Experience with Direct Pay under Section 6417 is preferred but not required; however, firms without such experience must clearly describe their approach to supporting Direct Pay compliance and filing.

Project Description

NGEMC plans, along with two other EMCs in Tennessee and North Carolina, to collectively deploy up to 5 MW (5,000 kW) and 20 MWh (20,000 kWh) of utility-scale battery energy storage systems that have a minimum storage duration of four (4) hours. NGEMC’s specific battery deployment is expected to be 1.4 MW (1,400 kW) and 5.6 MWh (5,600 kWh). The batteries will be deployed in three counties across the collective service territories of the three rural electric cooperatives. The project partners plan to help build and grow the “Battery Belt” in Appalachia by building demand and supply throughout the Region. Building demand involves all three co-ops deploying batteries that help them meet strategic objectives, sharing their experience with other rural electric utilities in Appalachia, and encouraging them to also deploy batteries. This increase in demand will drive battery manufacturers and their supply chain companies to build supply by establishing manufacturing and extraction operations in the Region.

NGEMC has received Appalachian Regional Commission (ARC) grant funds and will be applying for IRS Energy Tax Credits as matching funds for this project. Applicable ARC and IRS guidelines and requirements must be followed, including Prevailing Wage requirements and Domestic Content requirements, as well as all other federal and state requirements as applicable. The total project will range between $5-6 million, depending on final project configuration and eligibility for applicable tax credit enhancements.

This project is designed to build early demand for non-lithium, utility-scale battery technologies and, in doing so, stimulate new manufacturing capacity and supply chains across the Appalachian Region. By encouraging adoption of these innovative systems, the initiative aims to expand access to affordable, reliable, resilient, and energy-efficient infrastructure for both residents and businesses. At the same time, it supports a broader regional strategy to strengthen energy independence, reduce vulnerability, and proactively integrate alternative energy solutions into the utility landscape.

A partnership involving West Virginia University, Penn State University, and Tennessee Tech University will collaborate with rural electric utilities to evaluate a range of emerging non-lithium battery chemistries—including carbon-graphene, iron-air, and sodium-ion systems. These technologies are built on abundant, domestically sourced materials such as plastics, iron, and sodium. Unlike lithium, which is heavily demanded by the electric vehicle market, these chemistries offer utilities viable alternatives for stationary storage without competing with EV supply chains.

Applicable Federal Requirements

Prevailing Wage and Apprenticeship (PWA) Requirements

The NGEMC intends to apply for elective payment of the Clean Electricity Investment Credit available under Section 48E of the Internal Revenue Code of 1986, as amended, (the “Credit”) with respect to the property that will be installed and that the NGEMC intends to seek the additional credit amount allowed under Code Section 48E(a)(2)(ii)(III)(aa). In order to receive this increased credit amount, NGEMC must be able to demonstrate that it has complied with the applicable Prevailing Wage and Apprenticeship requirements set forth in Code Sections 48(a)(10) and 45(b)(8) as incorporated into the Credit by Code Sections 48E(d)(3) and (4), respectively, as those requirements may be amended by law (collectively, the “PWA Requirements”). Please see Appendix A for more information.

Domestic Content (DC) Requirements

The NGEMC intends to apply for elective payment of the Clean Electricity Investment Credit available under Section 48E of the Internal Revenue Code of 1986, as amended, (the “Credit”) with respect to the property that will be installed and that the NGEMC intends to seek this credit through the elective payment option under Code Section 6417. In order to receive the Credit through the elective payment option, NGEMC must be able to demonstrate that it has complied with the applicable Domestic Content requirements set forth in Code Section 45Y(g)(12) as incorporated into the Credit by Code Section 48E(d)(5), as those requirements may be amended by law (the “DC Requirements”). Please see Appendix A for more information.

North Georgia EMC is committed to providing all persons with equal access to its services, programs, activities, education, and employment regardless of race, color, national origin, religion, sex, familial status, disability, or age.

3. Schedule (Timetable)

The anticipated timetable is as follows (all times Eastern Time). NGEMC reserves the right to modify the schedule by addendum.

Screenshot

4. Proposal Submission Requirements

Proposals

Proposals shall be prepared on standard-size paper and limited to twenty (20) single-sided pages, excluding the cover and transmittal letter. Supporting materials (e.g., representative project examples) may be included as appendices and will not count toward the page limit.

Standard marketing materials or brochures should not be included unless directly relevant to the requested services.

All proposals must clearly demonstrate the Respondent’s ability to meet the minimum qualifications and evaluation criteria described in this RFP and Appendix C (Evaluation and Selection Criteria).

Minimum Qualifications (Required)

To be considered responsive, Respondents must demonstrate:

- Direct experience advising on Section 48E energy tax credits

- Direct experience advising on battery energy storage system projects

Firms that do not meet both of the above requirements will not be considered.

Experience with Direct Pay under Section 6417 is preferred but not required. Firms without Direct Pay experience must clearly describe their approach to supporting Direct Pay compliance and filing.

Proposal Content Requirements

Proposals shall include the following sections, in the order presented below:

1. Firm Overview and Relevant Experience

- Description of firm and relevant practice areas

- Experience advising public, cooperative, nonprofit, or tax-exempt entities

- Experience with federal funding programs (including ARC, if applicable)

2. Relevant Project Experience

Respondents must provide representative project examples demonstrating:

- Experience with Section 48E tax credits

- Experience with battery energy storage projects

- Experience with bonus credits (Prevailing Wage and Apprenticeship, Domestic Content, Energy Community, if applicable)

- Experience with Direct Pay (if available)

For each project, include:

- Project description and size

- Respondent’s role and scope of work

- Outcomes or results (e.g., credit claimed, compliance support provided)

- Client reference (name and contact information)

3. Key Personnel and Project Team

Respondents must identify the specific personnel who will be assigned to this engagement.

For each individual, provide:

- Name and role on this project

- Description of direct involvement in relevant Section 48E and battery storage projects

- Years of relevant experience

- Professional designation (e.g., partner, associate), for context only

Evaluation will prioritize direct project experience of assigned personnel over general firm experience or seniority.

4. Technical Approach and Project Execution

Respondents shall describe their proposed approach to delivering the Scope of Work (Appendix D), including:

- Approach to pre-procurement tax credit structuring and analysis

- Approach to RFP review and contract structuring

- Approach to vendor compliance evaluation and risk identification

- Approach to ongoing compliance monitoring through commissioning

- Approach to Direct Pay execution and audit readiness

If the Respondent does not have Direct Pay experience, this section must include a clear and detailed explanation of how Direct Pay requirements will be addressed. This explanation must address the Direct Pay process, including pre-filing registration, filing mechanics, and audit considerations.

5. Risk Identification and Mitigation

- Identification of key risks related to:

- 48E eligibility

- Battery project configuration

- Bonus credit qualification

- Direct Pay execution

- Proposed strategies to mitigate those risks

6. References

Provide at least three (3) references from similar projects.

7. Fees

- Proposed fee structure (hourly, fixed, or hybrid)

- Any assumptions or exclusions

8. Statement of Qualifications

Submission Requirements

Proposals must be submitted in accordance with the instructions provided in Sections 1-4 of this RFP. Include the Statement of Qualifications sheet with your submittal.

Evaluation Reference

All proposals will be evaluated in accordance with the criteria and weighting set forth in Appendix C – Evaluation and Selection Criteria

Proposal Due Date/Time: July 6, 2026, at 4:30 pm EST (Daylight Savings Time)

To be considered, proposals must be received by 4:30 pm EST (Daylight Savings Time) on July 6, 2026.

Submission Method: Electronic submittal via email to Paul Rudd, pruud@ngemc.com, AND Coty Burch, cburch@ngemc.com. No hardcopy submittal is required.

Include the RFP Title and RFP Number in the email subject line. Proposals must be received by 4:30 pm, July 6, 2026 EST (Daylight Savings Time). A representative of NGEMC will publicly read the names of the companies submitting proposals immediately following the closing date and time.

If NGEMC for any reason is unable to reach a final agreement with the finalist, NGEMC then reserves the right to reject such finalist and negotiate a final agreement with another finalist who has the next most viable proposal, and so on until an agreement can be reached with the finalist.

Late Proposals

Proposals received after the deadline will not be considered.

Irrevocable Offer

Any proposal submitted shall constitute an irrevocable offer for a period of 120 calendar days (or as otherwise specified in this RFP).

Incomplete Proposals

Incomplete proposals may not be considered if omissions are determined to be significant.

5. Evaluation and Award

NGEMC will evaluate proposals in accordance with the criteria and weighting set forth in Appendix C – Evaluation and Selection Criteria.

6. General Terms and Conditions

No Reimbursement of Proposal Costs

There are no expressed or implied obligations for NGEMC to reimburse responding companies for any expenses incurred in preparing proposals.

Ownership of Proposal / Public Records

Ownership of all data, materials, and documentation prepared for and submitted in response to this RFP shall belong exclusively to NGEMC and will be considered a public record subject to the Georgia Open Records Act, O.C.G.A. 50-18-70 et seq., unless otherwise provided by law.

Respondents should identify and mark information they believe qualifies for an exception (e.g., trade secret). NGEMC reserves the right to make the final determination on disclosure.

Certification of Understanding

By submitting a proposal, the Respondent certifies that it has fully read and understands this RFP and has full knowledge of the nature and scope of the work to be performed; the detailed requirements of the services to be provided; and the conditions under which the services are to be performed. Failure to do so will not relieve the successful respondent of its obligation to enter into a contract and to completely perform the contract in strict accordance with this RFP and any resulting contract.

Non-Collusion / No Kickbacks / Anti-Bribery / Competition

By submitting a proposal, all respondents certify that proposals are made in compliance with applicable Georgia laws on bribery and restraint of competition (including O.C.G.A. §§ 16-10-2 and 16-10-22). All respondents certify that their proposals are made without collusion or fraud; that they have not offered or received any kickbacks or inducements from any other person or party in connection with their proposals; and that they have not conferred with any NGEMC employee having official responsibility for this procurement transaction any payment, loan, subscription, advance, deposit of money, services, or anything of value of more than nominal value, present or promised, unless consideration of substantially equal or greater value was exchanged.

Debarment

Respondent certifies it is not currently debarred from submitting bids/proposals on contracts by any agency of the State of Georgia or the federal government, and is not an agent of a debarred entity.

Governing Law

This RFP and any resulting contract shall be governed by the laws of the State of Georgia; Respondent shall comply with applicable federal, state, and local laws and regulations. These include but are not limited to: 12 U.S.C. 1701 U and Clean Electricity Investment Credit requirements under Section 48E of the Internal Revenue Code of 1986, as amended, including Code Section 48E(a)(2)(ii)(III)(aa), with applicable Prevailing Wage and Apprenticeship requirements as set forth in Code Sections 48(a)(10) and 45(b)(8) as incorporated into the Credit by Code Sections 48E(d)(3) and (4), respectively, and Domestic Content (DC) Requirements under Code Section 45Y(g)(12) as incorporated into the Credit by Code Section 48E(d)(5). Please see Appendix B for applicable State and Federal laws.

Federally Assisted Project Civil Rights / Accessibility (If Applicable)

For federally assisted projects, NGEMC abides by Title VI (Civil Rights Act of 1964), Section 504 (Rehabilitation Act of 1973), Title II (ADA of 1990), Architectural Barriers Act of 1968, Fair Housing Act, and other applicable requirements. Include applicable clauses in the contract and require contractor compliance as relevant to the procurement.

Proposal as an Irrevocable Offer (Validity Period)

Any proposal submitted shall constitute an irrevocable offer for a period of one hundred twenty (120) calendar days from the proposal due date.

Ownership of Submittals; Public Information / Disclosure

Ownership of all data, materials, and documentation prepared for and submitted in response to this RFP shall belong exclusively to NGEMC.

Public Information: Information supplied by the respondent shall become public unless it falls within an exception (e.g., security information, trade secret information, or labor relations information). If the respondent believes any information that is not public will be supplied in response to this RFP, the respondent shall take reasonable steps to identify for NGEMC what data, if any, it believes falls within the exceptions. If the proposal data is not marked in such a way as to identify non-public data, NGEMC will treat the information as public and release it upon request. NGEMC reserves the right to make the final determination of whether data identified by the respondent as not public falls within the exceptions.

Contract Execution Deadline After Notice of Award

NGEMC reserves the right to award to the next most qualified firm if the selected firm does not execute a contract within thirty (30) days after notification of award.

Contract Form

The contract between NGEMC and the successful proposing firm will be on a form approved by NGEMC.

Reporting Requirements

The selected consultant will be required to provide regular reports, which will assist NGEMC in preparing quarterly project reports as required by the grantors, and will assist NGEMC with any applicable reporting to the IRS. The selected consultant will also assist NGEMC in preparing any other reports or project materials as required by the grantors.

7. Attachments / Required Forms (Checklist)

Include required forms as applicable: Debarment certification, Open Records/trade secret identification, E-Verify affidavit if physical services are performed, Statement of Qualifications, etc.

Appendix A – IRS Energy Tax Credit Requirements under Section 48E of the Internal Revenue Code of 1986, including Prevailing Wage and Apprenticeship Requirements and Domestic Content Requirements

Prevailing Wage and Apprenticeship (PWA) Requirements

Contractor understands that the NGEMC intends to apply for elective payment of the Clean Electricity Investment Credit available under Section 48E of the Internal Revenue Code of 1986, as amended, (the “Credit”) with respect to the property that will be installed and that the NGEMC intends to seek the additional credit amount allowed under Code Section 48E(a)(2)(ii)(III)(aa). In order to receive this increased credit amount, NGEMC must be able to demonstrate that it has complied with the applicable Prevailing Wage and Apprenticeship requirements set forth in Code Sections 48(a)(10) and 45(b)(8) as incorporated into the Credit by Code Sections 48E(d)(3) and (4), respectively, as those requirements may be amended by law (collectively, the “PWA Requirements”).

Respondent represents that it, and its Subcontractors, shall comply with the PWA Requirements, and any applicable Treasury Regulations; shall pay no less than the prevailing wage rate to all persons engaged in the performance of services; Contractor and Subcontractor, in accordance with applicable law, shall keep accurate payroll records; and that Respondent shall provide the [insert utility name] with such payroll records (including a written declaration that information in such payroll records is true and correct) as the client reasonably deems necessary to substantiate that Respondent and any Subcontractors have met the applicable PWA Requirements.

NGEMC reserves the right to request additional information and establish additional document retention policies should a contract be awarded.

Domestic Content (DC) Requirements

Respondent understands that the NGEMC intends to apply for elective payment of the Clean Electricity Investment Credit available under Section 48E of the Internal Revenue Code of 1986, as amended, (the “Credit”) with respect to the property that will be installed and that the NGEMC intends to seek this credit through the elective payment option under Code Section 6417. In order to receive the Credit through the elective payment option, NGEMC must be able to demonstrate that it has complied with the applicable Domestic Content requirements set forth in Code Section 45Y(g)(12) as incorporated into the Credit by Code Section 48E(d)(5), as those requirements may be amended by law (the “DC Requirements”).

Respondent represents that it, and its Subcontractors, has the ability at all times to comply with the DC Requirements, and any applicable Treasury Regulations, and that Respondent is willing and able to provide NGEMC with such records as the NGEMC reasonably deems necessary to substantiate that Respondent and any Subcontractors have met the applicable DC Requirements.

Appendix B – Applicable Federal and State Laws and Requirements

The applicable laws, regulations, and Executive Orders (classified in general by compliance area) include, but are not limited to:

General:

- The Housing and Community Development Act of 1974, as amended and as implemented by the most current HUD regulations (24 CFR Part 570)

- Annual Action Plan and State of Georgia CDBG Method of Distribution (MOD) for FFY 2021/2022 Consolidated Funds

- State Community Development Block Grant Program Regulations (24 CFR Part 570, Subpart I)

- Title 50, Chapter 18, Article 4, Official Georgia Code, Georgia Open Records Act

Financial Management:

- 2 CFR Part 200, Subpart F (formerly Federal OMB Circular A-133)

Civil Rights:

- Title VI – Civil Rights Act of 1964 and implementing regulations at 24 CFR Part 1.

- Section 109 – Title I – Housing and Community Act of 1974 and implementing regulations at 24 CFRPart 6.

- Title VIII of the Civil Rights Act, 1968 (Fair Housing Act), as amended

- Section 504 of the Rehabilitation Act of 1973, and the Americans with Disabilities Act of 1990

- Executive Order 11246 – Equal Employment Opportunity, as amended by Executive Order 11375, Parts II and III

- Executive Order 11063 – Equal Employment Opportunity, as amended by Executive Order 12259.

- Georgia Department of Community Affairs Civil Rights Compliance Certification Form

- Age Discrimination Act of 1975

- Executive Order 12432: National Priority to Develop Minority and Women-Owned Businesses

- Section 504 of the Rehabilitation Act of 1973 and implementation regulation (24 CFR Part 8)

- Section 104 of Title I of the Housing and Community Development Act of 1974 and the implementing regulations at 24 CFR Parts 5, 91, 92, 570, 574, 576, and 903

Other:

- Georgia House Bill 1079 as amended by House Bill 513 (O.C.G.A § 36-91-1 through §36-91- 95) Note: DCA has adopted this as the procurement regulation for ARC

- OCGA 13-10-90: Contracts for Public Works, Security and Immigration Compliance

- OCGA 50-36-1: Verification of Lawful Presence within the United States

- Federal Funding Accountability and Transparency Act (FFATA)

- Violence Against Women Act (VAWA, 34 U.S.C. § 12471 et seq.)

- IRS Energy Tax Credit Requirements under Section 48E of the Internal Revenue Code of 1986, including Prevailing Wage and Apprenticeship Requirements and Domestic Content Requirements.

Appendix C – Evaluation and Selection Criteria

Purpose

This appendix describes the evaluation criteria and scoring methodology that will be used to assess proposals.

The objective is to select a firm with demonstrated, project-relevant expertise in Section 48E and battery energy storage projects, and the ability to support the project through procurement, execution, and Direct Pay realization.

Minimum Qualification Screening (Pass/Fail)

Before scoring, proposals will be reviewed to confirm the following minimum qualifications:

- Demonstrated experience with Section 48E tax credits

- Demonstrated experience with battery energy storage projects

Firms that do not meet both requirements will not be evaluated further.

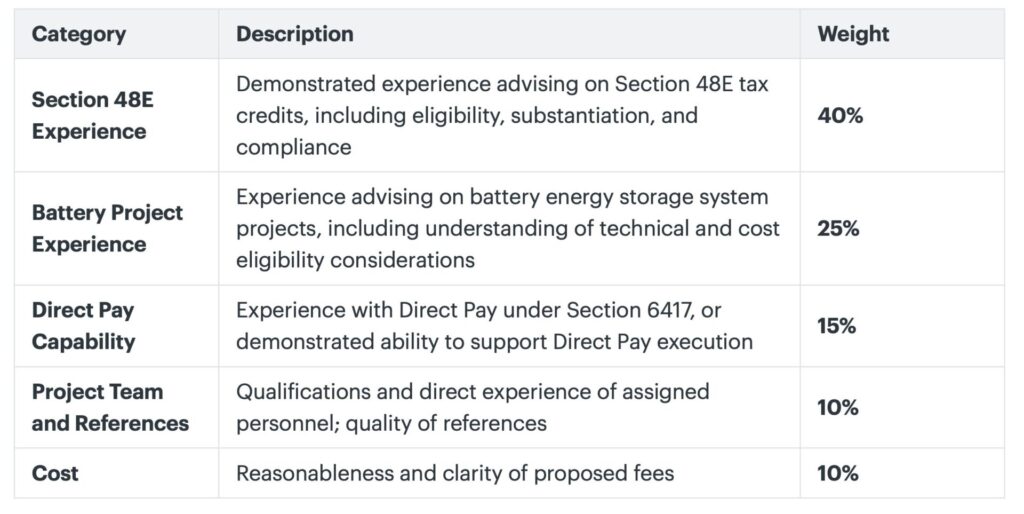

Evaluation Criteria and Weighting

Proposals that meet minimum qualifications will be scored based on the following criteria:

Evaluation Guidance

Section 48E Experience (40%)

Evaluators will consider:

- Depth of experience with 48E (not just general tax credits)

- Experience with eligibility, structuring, and compliance

- Demonstrated ability to support audit defensibility

Battery Project Experience (25%)

Evaluators will consider:

- Experience with standalone storage and/or hybrid systems

- Understanding of eligible cost components and system configuration

- Relevance to utility-scale or cooperative projects

Direct Pay Capability (15%)

Evaluators will consider:

- Experience with Direct Pay filings (if applicable)

- Understanding of:

- Pre-filing registration

- Filing requirements

- Coordination with tax preparers

- For firms without direct experience:

- Quality and credibility of proposed approach

Project Team and References (10%)

Evaluators will consider:

- Direct experience of assigned team members

- Relevance of prior work performed by those individuals

- Strength and relevance of references

Cost (10%)

Evaluators will consider:

- Clarity and structure of fees

- Alignment of cost with scope and level of expertise

Interviews

NGEMC anticipates conducting interviews with top-ranked Respondents to:

- Validate technical understanding of 48E and Direct Pay

- Confirm the experience of assigned team members

- Assess communication and project delivery approach

Selection

NGEMC intends to select the Respondent whose proposal is most advantageous based on the evaluation criteria above and to negotiate a final agreement.

Appendix D – Proposed Scope of Work (SOW)

Scope of Work

The selected firm shall provide legal due diligence and guidance to assist the electric cooperative (“Client”) in successfully securing and maximizing 48E direct pay tax credits for its qualifying energy storage project.

The scope of services should cover securing the 30% tax credit for meeting prevailing wage and apprenticeship requirements, and if applicable, +10 percentage points for meeting domestic content rules for iron, steel, and manufactured products, and/or +10 percentage points for being in an energy community. The major areas of support to accomplish this service include:

1. Pre-Procurement Structuring and Tax Credit Analysis

The Firm shall provide advisory services prior to issuance of the battery storage RFP to support project structuring and optimization of available tax credits under Section 48E and Section 6417.

This shall include:

- Evaluation of applicable credit structure, including Prevailing Wage and Apprenticeship requirements, Domestic Content eligibility, and potential Energy Community eligibility

- Development of high-level project scenarios comparing alternative project sizes and configurations and associated Direct Pay outcomes

- Assessment of whether the proposed project site may qualify as an Energy Community under current IRS guidance and identification of required supporting documentation

- Evaluation of timing and eligibility risks associated with Energy Community qualification over the project lifecycle, including risk of changes prior to placed-in-service

- Recommendations regarding whether to pursue Energy Community bonus credits and how such strategy should be reflected in the RFP and procurement approach

The Firm shall provide a written memorandum of findings to inform the Client’s decision regarding project scope and procurement strategy prior to issuance of the RFP.

2. Solicitation (RFP) Review and Structuring

The Firm shall review and advise on the Request for Proposals (RFP) and related solicitation documents for the battery energy storage system to ensure that all applicable requirements for qualification under Section 48E of the Internal Revenue Code and elective payment under Section 6417 (“Direct Pay”) are properly incorporated.

This shall include, at a minimum:

- Review and recommended revisions to RFP terms and conditions to ensure preservation of eligibility for the 48E tax credit and Direct Pay

- Identification and inclusion of required vendor obligations related to:

- Prevailing Wage and Apprenticeship (PWA) requirements

- Domestic Content requirements

- Documentation, certification, and record retention requirements necessary to substantiate the tax credit

- Recommendations for contractual provisions requiring vendor cooperation in providing data and documentation necessary for tax credit substantiation, filing, and audit defense

- Identification of potential compliance risks or structural issues that could adversely affect tax credit eligibility prior to issuance of the RFP

- The Firm shall also ensure that the structure and requirements of the RFP are aligned with the selected tax credit strategy, including whether Energy Community eligibility is assumed, required, or treated as optional.

3. Vendor Compliance Evaluation (Finalist Review)

The Firm shall perform a detailed legal and tax compliance review of the vendor proposals submitted in response to the RFP, with a particular focus on the one (1) to two (2) finalists identified by the Client.

This review shall include:

- Evaluation of each finalist’s proposed system, equipment, and project configuration for compliance with Section 48E eligibility requirements

- Assessment of each finalist’s ability to meet:

- Domestic Content requirements

- Prevailing Wage and Apprenticeship requirements

- Documentation and substantiation requirements necessary for Direct Pay

- Identification of risks that could impact the Client’s ability to claim or receive the tax credit, including risks of partial or full disallowance

The Firm shall provide a written compliance memorandum that:

- Summarizes findings for each finalist

- Identifies material compliance risks or deficiencies

- Provides a comparative assessment of finalists from a tax credit eligibility and risk perspective

This analysis is intended to inform and may materially impact the Client’s final vendor selection decision.

4. Vendor Contracting Support

The Firm shall review and advise on the final contract(s) with the selected vendor to ensure that all provisions necessary to preserve eligibility for the 48E tax credit and Direct Pay are incorporated.

This shall include:

- Review of contractual provisions related to:

- Compliance with PWA and Domestic Content requirements

- Documentation, certification, and reporting obligations

- Cooperation with the Client and its advisors in connection with tax credit substantiation and audit

- Recommendations for risk mitigation provisions, including remedies or protections in the event of vendor non-compliance

- Coordination, as needed, with the Client and other advisors to ensure alignment between procurement, construction, and tax credit requirements

5. Ongoing Compliance Monitoring and Advisory Support

The Firm shall provide ongoing legal advisory support throughout the project lifecycle to ensure continued compliance with Section 48E and Direct Pay requirements.

This shall include:

- Advising the Client during:

- Procurement

- Construction

- Installation

- Commissioning (placed-in-service determination)

- Review of material project changes, including change orders or scope modifications, for potential impact on tax credit eligibility or value

- Guidance on documentation collection, verification, and retention necessary to support tax credit claims and audit defense

- Assistance in identifying and addressing compliance issues as they arise during project execution

6. Direct Pay Filing and Audit Readiness Support

The Firm shall support the Client in preparing for and executing the Direct Pay process under Section 6417.

This shall include:

- Advising on pre-filing registration requirements

- Supporting preparation for tax credit filing, including coordination with accountants or tax preparers

- Ensuring that all required documentation and substantiation materials are complete and audit-ready

- Providing guidance on audit risk and defensibility of the tax credit claim

7. Deliverables

The Firm shall, at a minimum, provide the following deliverables:

- Written pre-procurement memorandum summarizing project structuring options, Energy Community eligibility, and Direct Pay implications

- Written recommendations on RFP language and structure, including alignment with the selected tax credit strategy

- Written compliance memorandum for vendor finalists

- Written recommendations on final vendor contract provisions

- Ongoing advisory memoranda or communications addressing compliance issues, as needed

- Support for Direct Pay filing readiness and audit documentation

Tax Credit RFP Questions & Responses

Q: Does the scope of work exclusively cover NGEMC’s specific deployment, or will the firm also coordinate advisory services across the partner co-ops’ entire rollout?

A: The scope of work will exclusively cover NGEMC’s deployment.

Q: The total project range listed was $5-6million, is this NGEMC portion of the project or is this the total cost of the entire project including the other two EMC’s?

A: This estimation is only NGEMC’s portion of the project.

Q: To what extent will the firm need to interface directly with the contractors and other partners to gather technical documentation for tax credit substantiation?

A: NGEMC will rely on the firm to provide direction and gather technical documentation for the tax credit substantiation.

Q: Is NGEMC planning to use an internal team or current external CPA for the actual Direct Pay tax filing, or should bidders include tax return preparation in their fees?

A: Bidders should include the preparation and filing of Form 990-T for the Direct Pay tax credits in their fees.

Q: Do you have access (current login credentials) to the ID.me business account for NGEMC? Is it known who the authorized user of that account is? Will the consultant be responsible for the pre-filing registration?

A: Bidders will be responsible for the pre-filing and submissions for the tax credits (Direct Pay).

Q: Has NGEMC ever filed a tax return with the IRS, such as a Form 990 or 990-T?

A: NGEMC is a 501(c)(12) cooperative and files a Form 990 and 990-T annually.

Q: If so, what is NGEMC’s established fiscal year-end?

A: NGEMC’s fiscal year is July 1st – June 30th.

Q: Do draft or existing contracts with contractors & subcontractors already include the necessary PWA and Domestic Content documentation requirements to ensure records are maintained in accordance with regulations and requestable by the advisory firm?

A: All required documentation related to domestic content requirements and prevailing wage and apprenticeship standards, etc. will be included in the vendor RFP and bid documents; the development and review of bid documents will be a task in which the selected tax credit firm will participate.

Q: Does NGEMC already have a shortlist of vendors capable of meeting Domestic Content requirements for the targeted non-lithium technologies?

A: Yes, NGEMC can provide the list of potential vendors upon request.

Q: What are the expected project start and completion (placed-in-service) dates?

A: Expected project start could be late 2026 or early 2027 and completed as late as 2029.

Q: Have the Appalachian Regional Commission (ARC) grant funds already been applied and approved? Will the application process be part of the project?

A: ARC funds have already been secured and approved for distribution.

Q: Are there any other forms (not including but like ARC) of funding (besides NGEMC funds) that will be received to support the project?

A: No other funding will be received.

Q: Will the consultant be responsible for calculating required basis reductions or tax credit offsets related to the use of ARC grant funds?

A: Yes, NGEMC will rely on the tax certificate advisor firm for this and other related services.

Q: Is or will the project be performed under a Project Labor Agreement (PLA)?

A: All Federal labor standards will apply including Davis Bacon and all related standards, and prevailing wage and apprenticeship standards. PLAs are not required.

Q: Due to recent law changes, many technologies viable under Section 48 must now be claimed under Section 48E. Is experience related to Section 48 applicable to this RFP?

A: Yes, please see Minimum Qualifications under Section 2. Purpose / Overview and Section 4. Proposal Submission Requirements.

Q: What percentage of the project does the North Georgia EMC expect to be funded by the Appalachian Regional Commission (ARC)?

A: 60% in ARC grant (~$3M) and 40% in tax credit (direct pay)(~$2M).

Q: What is the proposed ownership structure of the battery storage system between the North Georgia EMC and the three rural electric cooperatives?

A: Each cooperative will only own the battery installed on their system. NGEMC will exclusively own and operate the system located in Murray County.

Q: What is the expected start and end date for the construction of the battery storage project?

A: Start: Late 2026/ Early 2027, End: as late as 2029.

Q: What is the expected/planned amount of contractors/subcontractors to be utilized for the construction of the battery storage project?

A: TBD.

Q: When was, or will the construction contract be signed?

A: Construction contract has not been drafted.

Q: Have any material procurement, site work, or binding commitments occurred to date? If so, please describe.

A: No procurement or site work has occurred.

Q: Please confirm if you need assistance with preparing and filing the Form 990-T.

A: Yes, NGEMC will need assistance with filing for the Energy Tax Credits (Direct Pay) on Form 990-T.

Q: Please provide addresses or general area where the BESS system will be installed.

A: The battery will be installed at 4329 Hwy 411 S, Chatworth, GA, 30705.

Q: Please provide general timeline of activities for the BESS system.

A: Bidding and selection of contractor for site prep (~3 months), Site Prep (~1 month), Install the batteries (~1 month), Commission and start of operation of the batteries (~2 weeks). Start times for each goal are to be determined once appropriate contractors have been selected.

Project Name: Building the Battery Belt in Appalachian Georgia, project number MU-22018-2.

Project Location: The battery will be installed at 4329 Hwy 411 S, Chatworth, GA, 30705.

Project Commission Date: TBD.

Will you own the project once placed in service: Yes, will be owned 100% by NGEMC.

Type of Energy Project (wind, solar, CHP, etc.): Battery Storage.

Project size in terms of capacity: 1.4 MW / 5.6 MWh, 4-hour.

Estimated Project Cost: $5-6 million.

Primary contractor name: Contractor has not been decided.

Estimated number of contractors (EPC plus sub-contractors): TBD.

Do you have any Federal grants on the project: ARC grant to fund 60% of project.

Will you be financing with tax-exempt debt: NGEMC is a 501(c)(12) tax-exempt electric cooperative.

Number of primary equipment manufacturers: TBD.

Main manufacturers for project: TBD.